| |

| Courtesy Alteryx. |

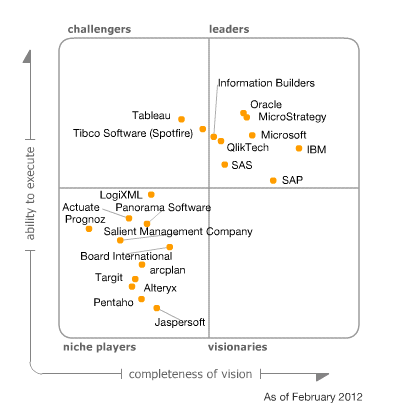

- 40+% of those rated are "leaders". One can only imagine how populous the "followers" box must be.

- 90+% of those rated are in half of the categories. Not exactly exploring the studio space on this graph, huh?

- There hasn't been a visionary in the business intelligence space since 2009 (there were 2 back then). Seems like a real growth opportunity.

| ||

| 2012 courtesy of Tableau. |

|

| 2011 courtesy of The Dashboard Spy. |

This does leave us with a rather interesting situation where solutions that were formerly considered departmental (tools like Tableau, Qlikview, and Tibco) might now be tasked with meeting enterprise needs. Clearly the price tag is attractive, but I have a feeling that all of the same reasons keeping large enterprises from going to the cloud (maturity, FUD, and the difficulties in extending and customizing solutions) are going to keep these smaller vendors serving marketing or HR while Cognos and BusinessObjects present the majority of data within most organizations.

In the end, I think Gartner's Magic Quadrant continues to serve the purpose it always has, which is a security blanket for those in procurement who won't buy any software that isn't at least mentioned. Only time will tell if that security blanket is getting a little thread-bare now that a vendors presence on here could mean they could be a safe bet for a large enterprise solution, a small or medium-sized enterprise solution, or even a departmental solution.

For an SAP-specific slant, please check out Dallas Marks's thoughts.